January 2014, Vol. 241 No. 1

Features

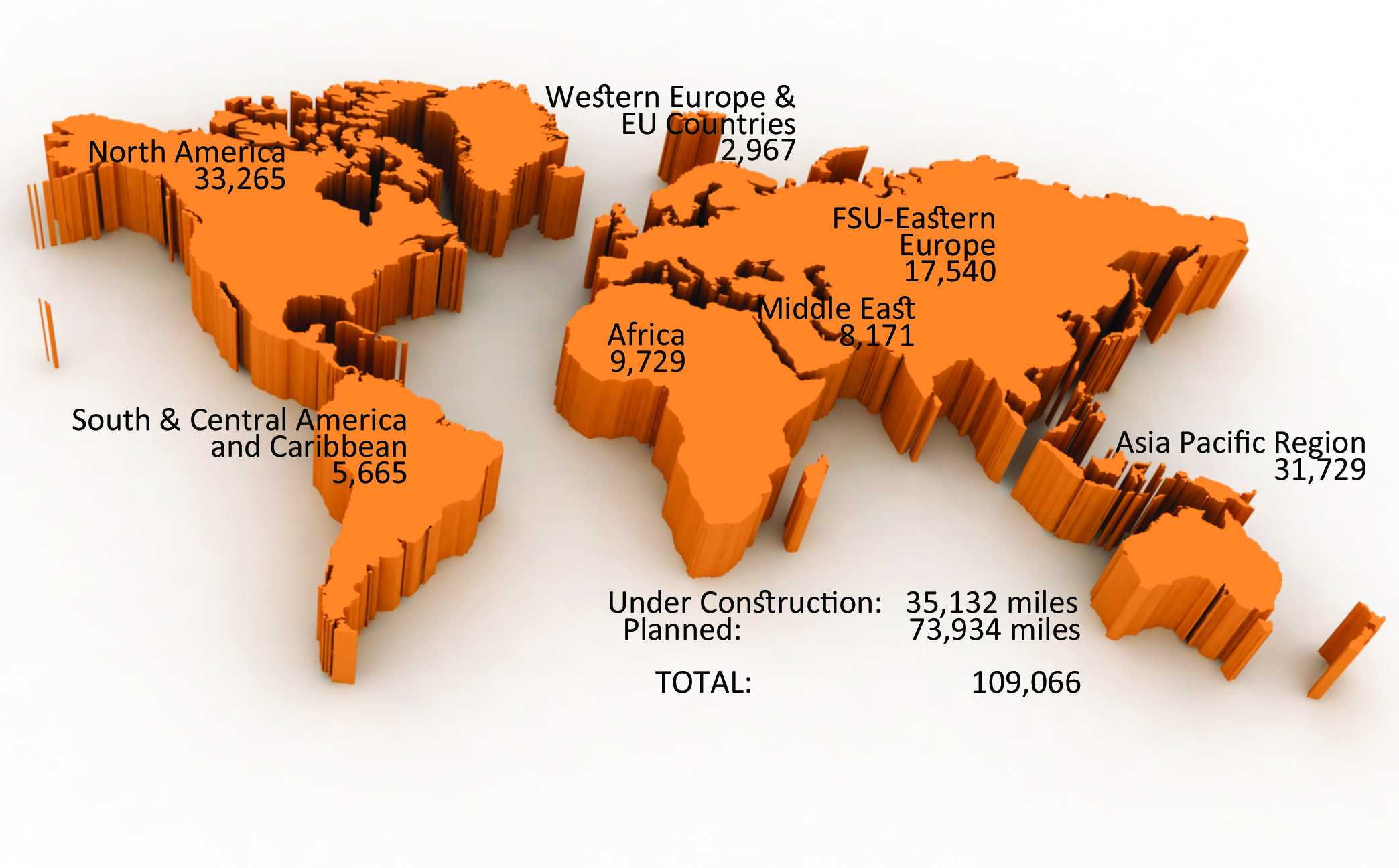

P&GJs 2014 Worldwide Construction Report

P&GJ’s 2014 survey figures show 109,066 miles of pipelines are planned or under construction worldwide. Of these, 73,934 are in the planning and design phase, while 35,132 are in various stages of construction.

The following looks at pipeline miles in the seven basic regional groups (see map) discussed in the report: North America – 33,265; South/Central America and Caribbean – 5,665; Africa – 9,729; Asia Pacific – 31,729 ; former Soviet Union and Eastern Europe – 17,540; Middle East – 8,171; and Western Europe and European Union – 2,967. More information can be found in P&GJ’s sister publication, Pipeline News.

North America

Increased shale gas production in the U.S. continues to boost mileage of new and planned pipelines. A recent U.S. Energy Information Administration report showed several pipeline expansion projects expected to begin service this winter to increase natural gas takeaway from the Appalachian Basin’s Marcellus Shale, where production has risen significantly the past two years.

According to the report, the expansions expected in-service through 2015 will add at least 3.5 Bcf/d of capacity to New York/New Jersey and Mid-Atlantic markets. Additionally, the capacity of pipelines to be installed from the Eagle Ford by 2017 exceeds expected production and will similarly ensure consumers’ stable supply.

Also projecting a major upturn in North America pipeline construction is Douglas Westwood’s (DW) most recent Pipeline Database Service, which identifies $22 billion worth of expenditure for the construction of more than 23,000 miles of pipeline from 2014-2020.

According to DW, more than 1,100 miles of transmission pipelines relate to the transportation of Permian crude and are planned to be built by the end of 2014. The report notes that Enbridge’s Flanagan South is under construction, intended to relieve the Cushing crude oil glut, along with TransCanada’s Gulf Coast Pipeline, and the twinning of the Seaway Pipeline owned by Enbridge and Enterprise Products Partners.

Moreover, it points out many companies are reversing existing pipelines to divert crude that would otherwise flow to Cushing, OK. Magellan Midstream, for instance, reversed a segment of its Longhorn Pipeline last year and plans to spend $55 million for a 50,000-bpd expansion this year.

No less striking, according to the report, is growth in the Marcellus Shale, which has risen to 18% of U.S. dry gas production. On paper, its share could rise to 25% by 2017, an increase of 6 Bcf/d from current levels. On top of this comes the Utica Shale, which pipeline operators are now treating as a play with Marcellus-scale potential.

Mexico

Mexico plans an $8 billion investment to expand its natural gas pipeline system that could be fueled by the South Texas and Eagle Ford plays in the U.S.

NET Midstream’s affiliate, NET Mexico Pipeline Partners was issued a Presidential Permit by FERC, which allows for border crossing facilities at the international boundary between the U.S. and Mexico.

NET Mexico will build a 124-mile, 42-inch and 48-inch natural gas pipeline system to the international boundary, with associated compression. The pipeline will transport gas from nine interconnects at the Agua Dulce Hub in Nueces County, TX to a point near Rio Grande City in Starr County to begin service in December.

Canada

Enbridge Inc. has been selected by the Fort Hills Partners (Suncor Energy Inc., Total E&P Canada Ltd. and Teck Resources Limited) to develop a $1.6 billion pipeline to transport crude under long-term commitments to Enbridge’s mainline hub at Hardisty, Alberta. The 36-inch, 228-mile Wood Buffalo Extension Pipeline will have initial capacity of 400,000 bpd, expandable to 800,000 bpd. Construction will run from the summer 2015 to spring 2017.

Enbridge is also involved in extending the Woodland Pipeline south from its Cheecham terminal to its Edmonton terminal, connecting with Edmonton-area refineries and export pipelines. With the Woodland Pipeline Extension Project, Enbridge is building more than $4.3 billion in infrastructure to service Alberta oil sands producers. The projects are expected in service by 2015.

Caribbean/South & Central America

Saipem won $500 million in contracts for offshore engineering and construction contracts in South America. Cardon IV, a 50/50 joint venture between Eni and Repsol, has commissioned work for the Perla EP project in the Gulf of Venezuela. This involves transportation and installation of a hub platform and two satellite platforms; a 42-mile, 30-inch offshore export pipeline; two 14-inch clad infield flowlines; other infield cables; and related tie-in operations. Most of the work will be performed by the Saipem 3000 and Castoro 7 vessels.

Petrobras awarded Saipem the Sapinhoa Norte and Iracema Sul project in the Santos Basin presalt region, 186 miles offshore Rio de Janeiro and São Paulo, Brazil. The work includes engineering, procurement, fabrication and installation of two offshore pipelines. Related terminations will be installed in the Sapinhoa Norte and Iracema Sul at depths of up to 7,218 feet.

Africa

Several African nations continue to deal with pipeline theft, ongoing threats to oil and gas workers, and an uncertain regulatory environment.

Technip is working under contract to Total E&P Congo on two developments: Moho Phase 1bis and Moho Nord, located off the coast of Congo, will install 143 miles of rigid pipelines, 143 miles of flexible pipes, 31 miles of umbilicals, 50 subsea structures and other components and rigid jumpers. First oil is expected in 2015 and 2016, respectively.

Technip also won two contracts from Tullow Ghana Ltd. for the TEN project off the coast of Ghana. Completion is expected in the second half of 2016.

Also in Ghana, Aecom Technology Corp. won a $15.6 million contract for the Western Corridor Ghana National Gas Infrastructure Development project. The project includes a 27-mile shallow-water pipeline section, a gas processing plant, a 68-mile pipeline onshore pipeline, a 46-mile onshore lateral, a natural gas liquids exports system and other infrastructure.

Still in the planning phase is the Trans-Saharan Gas Pipeline promoted by the Nigerian National Petroleum Company and Algeria’s Sonatrach. The 2,565-mile project would initially take 20 Bcm/y of gas from the Niger Delta region through the Republic of Niger to Algeria’s Beni Saf export terminal on the Mediterranean Sea. Experts warn the pipeline will be prone to attacks from terrorists and gangs. Nevertheless, the pipelines is scheduled to be in service by 2016.

Asia Pacific

China National Petroleum Corp. (CNPC) is constructing the third West-East Gas Pipeline. The 4,522-mile system consists of one trunkline, eight branches, three gas storages and an LNG station. It will cross 10 provinces and transmit 30 Bcm/y. Completion is expected in 2015.

CNPC has proposed the fourth and fifth West-to-East Gas pipelines, both in the planning stages. Both pipelines are expected to have 45 Bcm/y of capacity.

Also in China, Sinopec is involved in a coal-to-gas plant project in Zhundong that could result in 4,971 miles of gas pipeline being built. The $11.3 billion project is scheduled for completion in 2021.

Off Sabah, Technip is working for Sabah Shell Petroleum Co. Ltd. on subsea pipelines for the Malikai deepwater project. The contract includes transportation, installation and pre-commissioning of a 31-mile, 8-inch gas pipeline and a 34-mile 10-inch liquids pipeline, including catenary risers. Completion is expected in 2015.

Indonesia’s state-owned Pertamina signed a contract with Cheniere Energy’s subsidiary Corpus Christi Liquefaction to purchase 0.8 Mtpa of LNG from the export facility under development near Corpus Christi, TX. Deliveries are expected in 2018.

In India, Punj Lloyd is working on the Dahej-Hazira Pipeline for ONGC and the Dabhol-Bangalore Pipeline and the Kochi-Koottanad-Bangalore-Mangalore Pipeline Phase II for GAIL.

ONGC has also contracted Punj Lloyd for the design and installation work on the B-127 Cluster Pipeline off western India, where 72 miles of rigid subsea pipelines in nine segments are being installed and existing buoy moorings relocated. Also planned is installation of new pipeline end manifold on four existing platforms.

The Petroleum and Natural Gas Regulatory Board authorized Gujarat State Petronet Ltd. to proceed with three natural gas pipelines in India, totaling about 2,485 miles. The first pipeline (984 miles) will run from Mallavaram to Bhilwada, the second (1,025 miles) from Mehsana to Ghatinda and the third (447 miles) from Bhatinda to Jammu-Srinagar. Total capacity is 76.25 MMcm/d. GSPL has three years to complete the three pipelines.

Australia/Papua New Guinea

LNG developments continue to be the focus in Australia with Queensland alone accounting for five such projects now well along in planning and development:

Queensland Curtis LNG (QCLNG) – owned by the Queensland Gas Company QGC (a BG group company); Gladstone LNG (GLNG) – a joint venture between Santos Ltd, Petronas, Kogas and Total; Australia Pacific LNG (APLNG) – a joint venture project among Origin, ConocoPhillips and Sinopec; Arrow LNG – a joint venture between Shell and PetroChina; and Gladstone LNG Fishermans Landing – a joint venture between LNG Limited and Huanqiu Contracting and Engineering Corp. HQCEC (wholly owned subsidiary of China National Petroleum Corp.

The Queensland Curtis LNG (CLNG) project is progressing toward a 2014 startup. Queensland also has two proposed projects by Sun LNG (Sojitz Corp.) and Impel (Southern Cross LNG).

In Papua, New Guinea, Esso Highland, a subsidiary of ExxonMobil and operator of the PNG LNG project, is on track for the first LNG delivery later this year. At completion, more than 435 miles of pipeline will link Highlands gas to a liquefaction, storage and marine facility 12 miles northwest of Port Moresby. About 6.3 mtpa of LNG will be shipped to the Asian market.

Western Europe & EU Countries

Several Western European countries, including the UK and Norway, are benefiting from record investment in new developments and infrastructure improvements.

BP, ConocoPhillips, Chevron and Shell, are involved in the second phase of a £4.5 development on the Clair field, which lies 47 miles west of the Shetland Islands. The project will comprise two bridge-linked platforms and pipeline infrastructure connecting to processing facilities on Shetland. Installation of topsides takes place in 2015 with production expected in late 2016.

The second phase – Clair Ridge – is designed to produce until 2050 with the capability to produce 640 MMbbls of oil over a 40-year period. Peak production will be about 120,000 bpd.

On the Norwegian Continental Shelf, Lundin Petroleum is developing the Edvard Grieg field. The $4 billion project features a platform to receive and process hydrocarbons. A dedicated pipeline will be laid from the platform to the existing Grane Oil Pipeline for export to the Sture oil terminal. Similarly, a dedicated gas pipeline will be laid to the SAGE transport system on the UK shelf for export of rich gas to St. Fergus in Scotland.

First production from Edvard Grieg field is expected in late-2015 with a gross peak of 90,000 bopd and 1.5 million standard cu m/day of gas anticipated.

The development of the Johan Sverdrup field is planned by Statoil in 2018. The field is 87 miles west of Stavanger in 110 meters of water. Plans call for construction of a 170-mile oil pipeline linked to the Mongstad terminal in Bergan. A 103-mile gas export pipeline from the field to Statpipe for further transport to the Kårstø processing complex north of Stavanger is also expected.

Poland’s Gaz System has several gas pipelines in the planning phase and awaiting development decisions. The cross-border Poland-Slovakia pipeline would connect the gas transmission systems of the two countries and extend the Poland-Czech Republic pipeline. The European Commission is co-financing feasibility studies for both projects.

This cross-border gas pipeline would connect the gas transmission systems of Poland and Slovakia, giving Poland access to supplies from the Southern Gas Corridor. The Polish-Slovak link would have capacity of up to 5 Bcm/yr.

Poland is also working on a LNG terminal project in Swinoujscie with deliveries scheduled to begin in 2015.

Middle East

The focus in the Middle East is on boosting exports to Europe and the Asia Pacific region. Far East Asia received about 54% of Saudi Arabia’s crude oil exports in 2012 as well as the majority of its refined petroleum product and NGL exports.

Just as Saudi Arabia is working to increase exports, other Middle East countries are gearing up as well.

The National Gas Company of Iran is working on its ninth cross-country gas pipeline to increase exports to Turkey and Europe from the western regions of the country. The $10 billion, 932-mile-long Friendship Pipeline will transport 110 MMcf/d of Assalouych gas to Damascus from the Iranian South Pars field in the Persian Gulf.

In Iraq, SNC-Lavlin Group is involved in front end engineering and design of a 1,043-mile oil pipeline from Basra to the Red Sea port of Aqaba, bypassing the Strait of Hormuz. The Iraqi oil ministry reported the first phase of the pipeline will export 1 MMbopd from Basra. The second phase will export 125 MMbopd to the Syrian Banias port in the Mediterranean.

Also in Iraq, China National Petroleum Corp. began work on the second phase of the three-phase Halfaya project. The first phase became operational in June 2012 and is producing 100,000 bpd of crude and 1.6 MMcm/d of natural gas. The second phase, scheduled to become operational at mid-year, includes 60 wells, a 169-mile trunkline and a 5 Mtpa crude processing center. Phase 3, with a production target of 600,000 bopd, is scheduled for completion by late 2016.

FSU / Eastern Europe

Not surprisingly, much of the activity in this region is focused on feeding Asia Pacific’s growing energy demand. Chinese and Japanese companies have shown willingness to invest in future FSU and Eastern European projects to ensure supplies. One example is a joint $5 billion effort by Tokyo Gas, Japan Petroleum Exploration, Nippon Steel and Sumkin Engineering to construct an 870-mile gas pipeline from Sakhalin to Ibaraki Prefecture. The project is expected to take five to seven years.

Located off Russia’s eastern shore, Sakhalin Island is the home of several large oil and gas fields. Areas are being developed in phases with Sakhalin I and II producing oil and gas. Continued growth is expected to come from the Odoptu and Arkutun-Dagi fields in Sakhalin Island. Odoptu began producing in 2010, and Arkutun-Dagi is expected to produce shortly.

Russian exploration companies and international consortia are involved in the development of the Sakhalin resources. Although all of the consortia have extensive export plans via LNG terminals and export pipelines to the mainland, there has been little progress beyond the first two developments on the island.

Work is progressing on Gazprom’s South Stream Gas Pipeline, designed for maximum annual throughput of 63 Bcm. Work began near Anapa in the Krasnodar Territory in December 2012. In October 2013, work on the Bulgarian section began. Gazprom broke ground on the Serbian section in November that will have the capacity to transport 40.5 Bcm/y. It stretches about 260 miles across Serbia. Construction of South Stream’s Hungarian section will begin in April 2015.

The first gas will be supplied via South Stream in late 2015. The gas pipeline will reach its full capacity in 2018.

A major focus of Gazprom is to expand large-scale LNG exports on the fast-growing Asia-Pacific market. A special-purpose company – Gazprom LNG Vladivostok – will implement the Vladivostok-LNG project. The design is being developed with third-quarter competition in mind.

The start of supplies from the first train is expected in 2018 and from the second train in 2020. The capacity of each train will reach 5 million tons a year. According to an industry source, Gazprom has chosen Worley Parsons as contractor for the initial front-end engineering and design for the plant.

Russia now has a share of 4.5% of the global LNG market, which is dominated by Qatar. Russia aims to double its share by 2020 with the production of between 35 and 40 million tons a year.

Rosneft and ExxonMobil selected CB&I UK and Foster Wheeler Energy as contractors for initial phase front end engineering and design for a proposed Russian Far East LNG project. The plant design capacity of the project is expected to be 5 mtpa. The liquefaction plant will receive natural gas feedstock from Rosneft’s reserves in the Far East and other Sakhalin gas resources. Rosneft and ExxonMobil intend to complete project design by the end of 2014.

Although still in the planning phase, the 540-mile Trans Adriatic Pipeline (TAP) to transport natural gas from the giant Shah Deniz II field in Azerbaijan to Europe reached a milestone with the signing of a trilateral Intergovernmental Agreement by officials with Italy, Greece and Albania to develop, construction and operate the TAP pipeline.

TAP will connect with the Trans Anatolian Pipeline (TANAP) near the Turkish-Greek border at Kipoi, cross Greece and Albania and the Adriatic Sea, before coming ashore in Southern Italy. AP’s routing is designed to bring gas supply to several southeastern European countries including Bulgaria, Albania, Bosnia, Herzegovina, Montenegro and Croatia.

Plans call for TAP to transport first gas from the Shah Deniz field to Europe in 2019. TAP’s shareholding is comprised of BP (20%), SOCAR (20%), Statoil (20%), Fluxys (16%), Total (10%), E.ON (9%) and Axpo (5%).

Comments