December 2014, Vol. 241, No. 12

Features

Saudis May Hold The High Card

Global oil demand will grow 1 MMbpd in 2014, or about 300,000 bpd more than the IEA’s latest forecast, according to ESAI Energy’s recently published Global Fuels Outlook. The report highlights discrepancies between ESAI Energy’s and the IEA’s forecasts for demand growth and provides an outlook on petroleum product markets – and spreads to crude – through 2016.

There has been plenty of bearish talk about petroleum product demand lately, ESAI Energy noted. Publication of the IMF’s October World Economic Outlook attracted considerable attention for downward revisions to economic growth, especially for 2014, which is forecast at 3.3% (the same as the two previous years). Similarly, the IEA’s monthly Oil Market Report has made steady downward revisions to its 2014 demand expectations, most recently lowering global oil demand to just 700,000 bpd, partly due to weak year-on-year demand growth in the fourth quarter. The IEA also revised down 2015 demand growth to 1.1 MMbpd.

In Global Fuels Outlook, ESAI Energy maintains that global oil demand growth should be roughly 1 MMbpd this year. And in 2015 and 2016, demand should increase by another 1.2 MMbpd each year, according to the report. ESAI Energy data and forecasts paint a less bearish picture of refined product demand growth in China. The report finds that Chinese LPG and gasoline demand are on track to grow 120,000 bpd and 210,000 bpd, respectively, this year, or a combined 150,000 bpd more than the IEA forecast for those two fuels.

The IEA is also predicting a decrease in China’s diesel demand in 2014, when ESAI Energy expects demand to be essentially flat relative to 2013. This is also the year-to-date trend in China’s diesel demand.

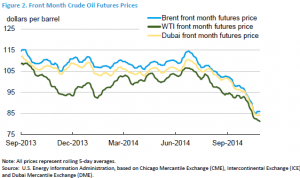

West Texas Intermediate crude futures are little changed this year as signs of economic recovery in the United States, the world’s largest oil user, counter slowing growth in emerging nations. Manufacturing and jobs growth in the world’s biggest economy surpassed forecasts in February, government data showed earlier this month.

The increase in global consumption will require a higher average level of crude this year from the Organization of Petroleum Exporting Countries (OPEC) than previously expected, according to the IEA. OPEC, responsible for about 40% of world oil supplies, will need to provide 29.7 MMbpd in 2014, or about 100,000 bpd more than anticipated in September. That’s 800,000 bpd less than the production in February.

OPEC’s 12 members boosted output by 500,000 bpd to 30.49 MMbpd in February led by a surge in Iraqi exports, which pushed OPEC’s production above its 30-million barrel ceiling for the first time in five months. Iraq’s production climbed by 530,000 bpd to 3.62 MMbpd, the most since 1979, while Saudi Arabia’s rose 90,000 bpd to 9.85 MMbpd.

Though expansion in demand next year will be accounted for by developing nations, the pace of growth in China and other emerging nations is slowing, the IEA said. United States demand “continues to show signs of strengthening,” it said. Tension between the West and Russia over Ukraine “has increased downside risk to the forecast” for global consumption, the agency said.

Unusually cold weather in the United States helped caused a “staggering” drop in oil inventories among developed nations, which fell by 13.2 MMbbls to 2.6 Bbbls in January, a month when they normally accumulate, the report showed. Supplies in the Organization for Economic Cooperation and Development were 154 MMbbls below seasonal average at the end of January, the widest deficit in more than a decade.

“An improving supply outlook partly offsets these recent draws,” with supplies from outside OPEC rising at the fastest pace since the early 1990s, the IEA said. Non-OPEC production, driven by the United States, Canada and Brazil, will climb by 1.7 MMbpd this year to 56.4 MMbpd.

“We think product demand growth will not decelerate in the fourth quarter, and that year-on-year stability in late 2014 will form the basis for more robust demand growth in 2015,” said ESAI Energy’s John Galante. “Weak underlying crude prices will also help drive demand growth in the years ahead.”

In terms of prices, especially for products like diesel and jet fuel, ESAI Energy believes its relatively robust global demand picture will offset some of the bearish pressure on spreads that is coming from big additions to supply. According to Galante, “Fundamentals are not weakening so drastically that the bottom will fall out of margins during the next two years.”

Notes Mark A. Plummer, owner, Chestnut Exploration Companies, when asked if oil drilling programs remain viable as crude prices fall, “The answer is an emphatic “Yes.”

“First, Bloomberg reports worldwide demand for crude oil demand continues to grow at 1.5% to a record 92.7 MMbpd and this growth will continue as the world economy recovers. As with any commodity, an increase in demand, absent a corresponding increase in supply promotes higher (or at least stable) prices. As such, we should not expect prices to fall precipitously while worldwide demand increases.

“Second, the significant tax benefits related to oil and gas exploration do not depend on crude prices. Rather, these tax benefits depend on drilling costs which include drilling equipment, materials, and labor. Finally, direct private placement drilling programs funded with limited partner cash contributions have no debt burden, which among other things, eliminates leverage, reduces risk and reduces the production necessary to derive a profit.

“While $80 a barrel crude presents a real threat to highly leveraged oil companies and countries like Venezuela, direct investment drilling programs remain viable at $80 a barrel and below crude prices,” he said.

How Low Can Oil Prices Really Go?

Oil price volatility returned with a vengeance in October amid worries of slower economic growth, weakening oil demand, an unexpected increase in Libya’s output and Saudi Arabia’s indication it would not cut output in the face of weaker oil demand. By the end of October U.S. oil prices continued to hover just above $80 per barrel for West Texas Intermediate (WTI).

The oil price decline is more a reaction to possible future weakness in oil demand than to a sudden change in supply and demand fundamentals. It is true short term demand is lower than expected, but the longer term outlook remains positive, according to Wood Mackenzie’s latest analysis.

“Current production in most areas of the world, including U.S. tight oil, is economic well below current oil prices and not likely to be shut, except for a few unusual cases, such as U.S. extra heavy and ‘stripper’ well production,” said Ann-Louise Hittle, Head of Macro Oils for Wood Mackenzie.

Key Considerations

1) Wood Mackenzie expects the global economy to remain stable in 2015 and support oil demand gains. With demand continuing to grow, the projected strong increase in non-OPEC production can be absorbed in the market without causing further significant price declines. If market concerns about the economy materialize, prices could fall further as the market moves into an oversupply situation.

In a scenario in which global demand creeps up by only 500,000 bpd in 2015, there would be little recovery from current prices levels, or possibly significant further downward pressure on prices if OPEC producers do not take action to cut output. “We are not ruling out a production cut from OPEC but wanted to examine what the oil price floor would be if the group did not act to support the market.”

2) U.S. tight oil break even prices are a good short-term measure of how low prices can go as producers can adjust and shift their drilling programs relatively quickly. Using this metric, Brent prices are unlikely to be sustained below $80 per barrel in the shorter term – beyond 2015 – because of the effect on U.S. tight oil growth.

3) The bulk of new U.S. tight oil developments are economic down to $70-75 per barrel (WTI) or $80-85 for Brent. At $70 for WTI, (Brent near $80) the U.S. tight oil sector would lose about $15 billion in cash flow in 2015. This equates to a relatively minor 150,000 bpd in lost production growth in 2015, if fully cut from drilling budgets. If however, prices fall below this threshold and remain there for much of 2015, about 0.6 MMbpd of U.S. tight oil supply growth would be under serious threat by the end of next year, a volume that would increase each year with low prices.

4) The loss of these growing volumes would help move the market back into balance and stabilize oil prices. In addition, another influence on supply from low prices would be underway. Projected growth or development of future oil supply will also become curtailed by low oil prices. Development of high-cost future supply or what is called marginal oil supply is at risk in a low oil price environment, but the impact of this occurs over a three-to-five year time frame. The U.S. tight oil market is the most flexible because of the scope for relatively rapid changes in production levels.

Rice Experts On $3 Gas Prices

Goldman Sachs cut its price forecasts for the first quarter of 2015 from $100 a barrel to $85 a barrel for Brent, the global benchmark, and from $90 a barrel to $75 a barrel for the U.S. benchmark. The bank sees prices dipping an additional $5 a barrel in the second quarter. Many investors think prices have further to fall. “We could see $70 here. I don’t think that’s out of the question,” said Robin Wehbé, portfolio director at Boston Company Asset Management, a unit of Bank of New York Mellon.

Rice University energy experts ventured their perspectives on Goldman Sachs’ projections, based on rising U.S. production and OPEC’s reluctance to cut production. While sub-$3 a gallon gas prices might be good for drivers, it could have less desirable effects on Houston and U.S. producers, stock prices and the economy.

Ken Medlock, senior director of the Center of Energy Studies at Rice University’s Baker Institute and lecturer in economics, said: “Falling oil prices can pressure higher-cost production ventures around the world, including some shale-directed drilling. But short-term movements are not the harbinger of a substantial pullback.

“The drop must be sustained for there to be a significant impact on drilling activity. To fully understand the implications of lower oil prices, it is important to understand the drivers. Namely, if prices are lower due to demand destruction or a negative global economic outlook, then things could get ugly across a number of sectors. But, if prices are lower due to strong supply growth and a strengthening dollar, then the story is different. In particular, regional economies in energy-producing regions, such as Texas, will remain vibrant due to their diversity, and demand pull will remain sufficient to place a reasonable floor under oil prices that reflects a healthy upstream outlook.”

William Arnold, professor in the practice of management at Rice University’s Jones Graduate School of Business, said: “The past three years have seen massive portfolio shifts and corporate restructuring – separating upstream and downstream companies, shifting from international to domestic assets, dry gas to liquids, and selling assets to pay down debt.

“Oil and gas companies are often torn between the challenge to replace reserves and the returns on those assets. Much of the focus lately has been on cost leadership and operational efficiency. This will get laser-like attention in the current environment. How companies respond will provide insights into their portfolios – which assets are in fact viable with sustained lower prices.”

Jim Krane, the Wallace S. Wilson Fellow for Energy Studies at Rice University’s Baker Institute, said: “The Saudis are contributing to the drift in prices. A lot of non-OPEC producers, including those in the United States and Canada, have been assuming that the Saudis would prop up prices by cutting back on production. They were banking on an understanding that Riyadh needed to maintain high oil prices to fund social spending that would reduce the appeal of an Arab Spring-style uprising in Saudi Arabia.

“But the Saudis have come to the conclusion that they now need to defend their share of the market, regardless of price. Instead of cutting back, the Saudis have maintained production and even given discounts to some importers. They’re essentially calling the bluff of high-price producers. Do you really want to invest in a multibillion-dollar scheme in the Arctic when oil markets are brimming with excess crude?

“Since Saudi production costs are so low, their willingness to accept lower prices sends a chilling signal to folks who cannot get oil out of the ground so cheaply. If it’s a race to the bottom, the Saudis have demonstrated in the past – in the late 1980s – that they can win, and that they’re willing to suffer to establish market discipline.

“This time around, the ruling sheikhs in Riyadh are probably only hoping that a little Halloween scare is all the market needs. Saudi Arabia and the other OPEC countries still have huge spending commitments at home, which means they will have to pay attention to prices again at some point.”

Comments