April 2018, Vol.245, No.4

Features

Choosing Brown vs. Green: Seeking Lower Risk, More Certainty

By Richard Nemec, Contributing Editor

When the proposed Atlantic Sunrise Pipeline project from the Marcellus shale gas deposits in Pennsylvania was stalled last year in a legal quagmire that has engulfed a number of high-profile, multi-billion-dollar greenfield projects, the Federal Energy Regulatory Commission (FERC) – operating at full strength for the first time in the Trump administration – attempted to unknot the permitting conundrum by approving two relatively benign looping projects.

While seeming small in nature, the action loomed large in today’s increasingly complex regulatory and financial process for building new energy infrastructure.

A week later, at his first meeting as the U.S. Senate-confirmed head of FERC, Chairman Kevin McIntyre indicated he wanted to open up for review the federal process for building new energy infrastructure. The timing is important, given the fact that building new, so-called "greenfield" projects, has become a maze of court filings at a time when "infrastructure" enjoys bipartisan support.

McIntyre’s opening thoughts on the issue deserve some serious consideration, coming when the use of so-called "brownfield" or expansion projects, are taking center stage as a logical outgrowth of the problems facing the construction of any totally new infrastructure in the energy space.

"We collectively as a government institution, owe it to all concerned to take a look at our processes and policies from time to time and say, ‘Is there any way we can improve them?’" said McIntyre last December as he assumed the lead role at FERC.

The elements of McIntyre’s desire to review the federal permitting processes illustrate the 2018 infrastructure market dynamics marked by the fallback position of brownfield vs. greenfield in capital development. In an era in which the traditional regulatory steps seem to be broken, McIntyre and his FERC colleagues face a major challenge. In late February, a FERC spokesperson said the federal regulators had taken no action so far to address the chairman’s outline for the national reviews. Ultimately, they need to address his concerns.

"I am approaching this topic with an open mind," McIntyre said, in wrapping up a late December meeting at the commission offices in Washington, D,C. "I want the staff and the commission to take a fresh look at all aspects of the issue of permitting. I have had some early discussions on the matter with my fellow commissioners and am delighted by their enthusiasm on the projects."

In early 2018, FERC had yet to get its bureaucratic arms around the chairman’s obvious desire to rescue the state of energy infrastructure build-out in this year and beyond.

FERC’s decision to move ahead with looping came within little more of a week of an earlier decision to deny environmental groups’ requests to delay processing of the overall Atlantic Sunrise project, an important project for freeing the continuing constraints on moving Marcellus gas to the Northeast region. Williams’ Transcontinental Pipe Line Co. LLC (Transco) got FERC’s OK to construct two looping sections in north-central Pennsylvania and use adjacent contractor yards for the overall $3 billion, 198-mile interstate gas pipeline project.

Recent U.S. Energy Information Administration (EIA) statistics show the bulk of the pipeline projects in various stages from conception to construction are brownfield both in terms of numbers and volumes. EIA listed pipeline reversal or expansion projects as totaling 19 Bcf last year, while the lateral or new pipeline projects equated to 12.8 Bcf. This sets aside projects that have been designated as "on hold," said Matthew Hong, oil and gas research director at Morningstar Commodities Research.

"I’m not sure whether the absolute number of projects translates into a higher rate of brownfield projects vs. greenfield, but I do think there is a reason why brownfield projects are more attractive than greenfield projects currently," said Hong, citing continuing regulatory uncertainty brought on by legal challenges as a primary driver.

Adding the now talked about FERC review of the permitting process this year to the ongoing court and state regulator approaches, the uncertainty remains palpable for 2018, according to Hong, who has reviewed the environment for more reliance on brownfield infrastructure projects. "I think the uncertainty will continue to favor the pursuit of more brownfield projects than greenfield ones until these underlying issues are resolved."

Cathy Landry, the communications director for Washington, D.C.-based Interstate Natural Gas Association of America (INGAA) said that her membership is not expressing a preference, brown-vs-green, but she thinks companies "always opt for brownfield over greenfield when they have a choice; it’s a no-brainer, given rights-of-way issues, costs and timing."

Financing for interstate infrastructure projects is another driver. Hong notes that the brownfield projects are more likely to have lower capital return thresholds than greenfield undertakings. The brownfield projects already have gone through regulatory permitting processes. Thus, FERC’s process for the Atlantic Sunrise looping and compression project was simpler and more straightforward compared to the steps required for a new greenfield project.

"That doesn’t mean that there is no risk of brownfield projects being rejected," Hong said. "I do think the availability or likelihood of projects receiving funding is another factor behind the type of projects being pursued and their relative attractiveness [brown vs. greenfield]."

In Canada, early in February, the energy pipeline industry was raising concerns with the National Energy Board (NEB)’s review and proposed changes in national energy policy. The Canadian Energy Pipeline Association (CEPA) expressed concerns that uncertainty was being worsened by some of the changes.

"CEPA member companies that propose to invest in pipeline projects in Canada need a regulatory system that promotes clarity," a spokesperson for the group said. "There is serious risk that companies will invest their capital in other jurisdictions if faced with unacceptable uncertainty, costs and delays." Faced with added uncertainty in the rules, companies will gravitate to more brownfield investments.

"It is absolutely critical that the regulatory reform initiatives [announced in early February] do not add to the significant obstacles already facing our energy industry," CEPA warned the NEB.

At one point in mid-2017, Angus Rodger, the Wood MacKenzie consulting firms’ research director, noted that 11 of 15 infrastructure projects that were sanctioned at that point in the year were brownfield expansions on existing fields. Rodger told news media last year that the brownfield projects reflect lower capital expenditures (CapEx) per barrel and stronger project returns. The CapEx costs were down to $11/boe, compared to a $15/boe cost two years earlier, and internal rates of return rose from 11% to 15% for the brownfield projects over that same two-year span.

While the role of future rising interest rates and whether projects pencil out from a net present value (NPV) standpoint are problematic at best, whether infrastructure can attract adequate financing is still a major challenge. "The availability or likelihood of a project receiving funding is another factor behind the type of projects being pursued and the attractiveness of one versus another," Hong said.

Bigger brownfield projects exist, and the greenfield prospects from Atlantic Sunrise to Mountain Valley out of the Marcellus continue to dominate, but the bread-and-butter of faster track brownfield projects, such as the Southwest Louisiana project, a 900 MMcf/d reversal, and the 650 MMcf/d Wright Interconnect Project (WIP) help keep the U.S. oil/gas infrastructure build-out on track.

Some of this push forward with needed, smaller reversals and expansions moves along because of the utility sector’s backing, underwriting long-term contracts that help spring for financing of the brownfield projects.

In 2017, an industry-backed bill in Congress sought to speed up FERC’s natural gas pipeline review process by placing additional requirements on participating agencies. HR 2910, introduced by Rep. Bill Flores (R-TX), was passed by the House last July and sent on to the U.S. Senate. Drawing bipartisan support, a group of 20 trade associations – including INGAA, the American Petroleum Institute, the utility-driven American Gas Association, the Consumer Energy Alliance, the Independent Petroleum Association of America, the U.S. Chamber of Commerce and others – sent a letter in support of the legislation.

The trade groups promote the bill as a way to "improve interagency coordination" in natural gas pipeline reviews by strengthening "the role of the FERC as the lead agency" in following the guidelines set out in the National Environmental Policy Act (NEPA). The bill would also encourage concurrent reviews to help streamline the process, the groups wrote. "Unfortunately, the permitting process has become more protracted and challenging in recent years," they wrote. "We need a process that is fair, comprehensive and ensures common sense cooperation and timely decision-making."

Even with the pushes for change, observers in the industry don’t see the federal review process being anything other than multiple years in the making, and while the treatment of brownfield projects may remain an exception, there should not be a long list of changes in the treatment of new greenfield projects, one analyst reiterated in early 2018.

Tennessee Gas Pipeline Co. LLC’s (TGP) Southwest Louisiana Supply Project, adds an additional 295,000 Dth/d of firm transportation service on the pipeline’s 800 Line for delivery to an existing interconnection with Cameron Interstate Pipeline LLC in Cameron Parish, LA.

FERC green lighted the project for Kinder Morgan Inc.’s (KMI) TGP plans to construct a 2.4-mile, 30-inch pipeline lateral in Madison Parish, LA; a 1.4-mile, 30-inch lateral in Richland and Franklin parishes, LA; five meter stations; one new compressor station in Franklin Parish, and replace a gas turbine engine at an existing compressor station in Rapides Parish, capping a classic brownfield expansion/upgrade.

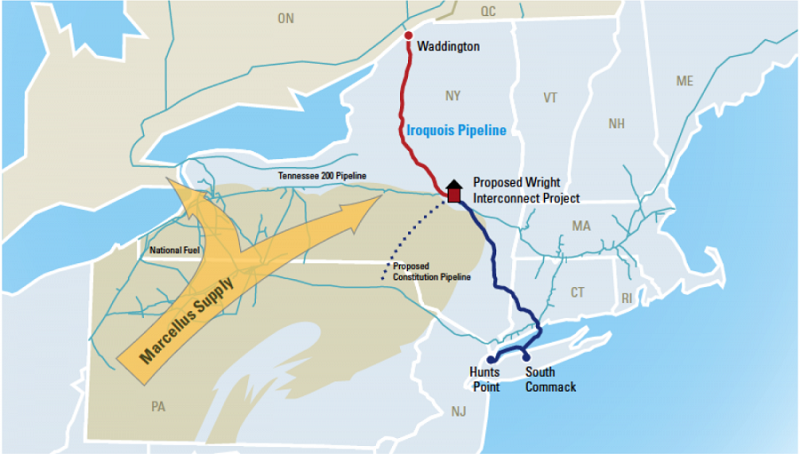

Following up on larger greenfield machinations, the Wright , or WIP project, proposes to expand the Iroquois Gas Transmission System’s existing compression and metering facilities in Wright, N.Y., as part of the proposed larger Constitution Pipeline project, enabling delivery of up to 650,000 Dth/d from the terminus of the Constitution Pipeline in Schoharie County, N.Y. into both Iroquois and the TGP systems under a 15-year capacity lease agreement with Constitution.

Much larger projects can be found on the EIA listing for brownfield development, but it is not clear how many of them are alive and active in 2018. They are not necessarily all moving forward, according to industry analysts and observers who monitor both the brown and greenfield projects.

In addition, there are many projects that are installing new pipe and compressors that essentially mimic existing rights-of-way and facilities: KMI and Enbridge Energy Partners LP in western Canada. KMI’s $5.3 billion Trans Mountain oil pipeline will nearly triple the existing line’s capacity to 890,000 bpd at least two sizable segments in which existing pipeline will be linked to new segments ranging from 30 to 42 inches.

As a brownfield development of sorts, Trans Mountain has Canadian federal approvals, but was bogged down most of 2017 with local opposition at the dockside end point of the oil line.

While everyone in Canada recognizes the provinces lack the power to overrule federally approved energy projects, British Columbia government officials nevertheless early in 2018 were threatening to block the pipeline replacement project by restricting the volumes of heavy Alberta oil allowed into B.C.

This is a case where the pipeline project from an engineering standpoint is straightforward, but from a permitting and socio-economic standpoint extraneous factors make it as complex as a traditional greenfield project. Citizen and local government push back has become a norm whenever infrastructure (brown or green) is involved.

A second similar brownfield type effort is Enbridge Partners’ enhanced pipeline reliability program on the southern part of its natural gas transmission system, stretching south from Chetwynd, B.C. to a point at the U.S.-Canada border near Sumas, WA. This is essentially an equipment upgrade project used to enhance operating safety, efficiency and reliability, according to the Enbridge engineers.

"It involves adding new compressor units at three existing stations along the pipeline system as well as upgrading existing pipeline crossovers and adding new crossovers at key locations," according to an Enbridge spokesperson. "The project is designed to increase efficiency and reliability along the southern portion of this natural gas transmission system in B.C."

In the first months of 2018 it is clear that continuing robust oil and gas production in North America will keep expansion of the existing valuable pipeline and relate infrastructure as top-of-mind for the industry.

This was clear on both sides of the Canada-U.S. border as giants like TransCanada and Energy Transfer Partners (ETP) eyed expansion of their existing Nova Gas Transmission Ltd. (NGTL) and Bakken Pipeline System networks, respectively. North America’s anticipated incremental production is part of the drivers for infrastructure expansion.

In Canada, Alberta’s expanding thermal oil sands plants require lots of natural gas, so NGTL is seeking NEB approval for a $166 million capacity expansion, the North Path Delivery Project, to serve the bitumen extraction region. North Path includes a 36-inch pipeline and two compressor stations to move gas from western Alberta and eastern B.C. With timely NEB approval, TransCanada was forecasting a November 2019 start for the expansion project deliveries.

In the United States, ETP kicked off March with an open season for its Bakken system that includes the Dakota Access Pipeline (DAPL) and the Illinois-to-the-Gulf-Coast Energy Transfer Crude Oil Co. (ETCO) pipeline. While the open season was primarily to soak up the unused capacity of the pipelines that deliver Bakken sweet crude to both Midwestern and Gulf refineries, ETP has acknowledged there could be incremental market interest that would necessitate expansion of the 570,000 bpd capacity.

North Dakota energy officials, who carefully chart all the movements and machinations of the Bakken producers, were anticipating continued boosts in demand this year for pipeline space to move the state’s growing production that has remained above 1 MMbpd.

The continuing narrow price differential spreads that were about $3/bbl early in March will keep pulling more barrels onto pipelines, said Justin Kringstad, director of the North Dakota Pipeline Authority, who has tracked of the monthly increasing flows of oil through DAPL since it launched operations in June 2017.

"I estimate it will take at least $5-$6-plus a barrel spread between Brent and WTI prices before any significant shift away from pipelines would occur," he said. P&GJ

Richard Nemec is a regular P&GJ correspondent based in Los Angeles. He can be reached at: renmec@ca.rr.com.

Comments