December 2018, Vol. 245, No. 12

Features

Contractor Competition Delivering Lower Costs to US Utilities

By James M. Seibert, Managing Partner, Chicago Energy Associates LLC

Electric and gas utility executives, and regulators are increasingly focused on the cost of the capital expenditures (capex) in transmission and distribution (T&D) infrastructure.

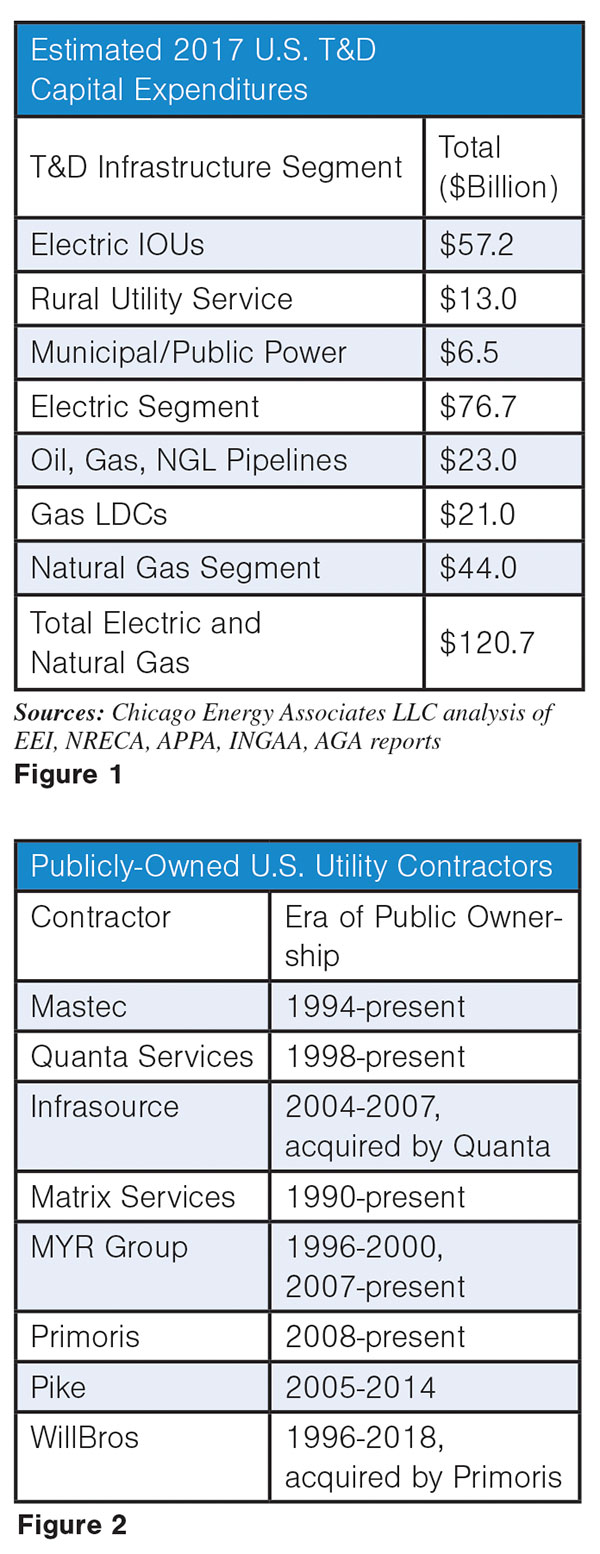

Total capex across the U.S. energy delivery complex is about $120 billion per year (Figure 1), and commonly more than three times larger than operations and maintenance expenses (excluding depreciation), and it seems to grow every year.

Consequently, many utility leaders are openly and appropriately questioning whether the industry’s construction contractors are exploiting the vigorous demand for T&D infrastructure to raise prices and profits to the detriment of current and future energy consumers.

Outsourced Capex

A very high proportion of utility T&D infrastructure is constructed by contractors rather than by the utility-employed workforce, who predominantly focus on system operations, maintenance, and emergency repair. The industry’s outsourcing rationale is compelling.

First, labor costs per man hour and per installed asset unit are typically lower from contractors because they deliver work through competitive pricing and often have lower wage, incentive, and pension costs.

Second, infrastructure construction is typically contracted on a fixed total cost or fixed per-unit cost basis, thereby shifting much of a project’s commercial and construction risk from the T&D infrastructure owner to the contractor. Third, a utility’s new and replacement capex workload often varies seasonally, year-to-year with economic growth, by skill or craft, and geographically. This diversity makes the logistics of a permanent, in-house construction workforce inefficient when compared to a contractor. Additionally, as a regulated industry, competitive bidding of construction activity provides regulators and the public with increased confidence that utilities are realizing the lowest practical cost for new and replacement assets placed in service and into the rate base.

The increased attention on construction expenditures and reliance on outsiders leads executives and regulators to seek a deeper understanding of their contractor’s business. They express a range of practical concerns about these contractors, including specifically whether recent construction demand growth is driving up costs (providing higher profits), whether ongoing consolidation of the contractor industry into ever larger firms is, likewise, reducing competition to increase prices, and whether the construction industry is committed to making the long-term investment in their own capacity to continue to serve the nation’s infrastructure needs.

Answering these specific questions with certainty requires a detailed financial analysis of the last two decades of public ownership of the major electric and gas T&D contractors through their annual SEC 10-K filings.

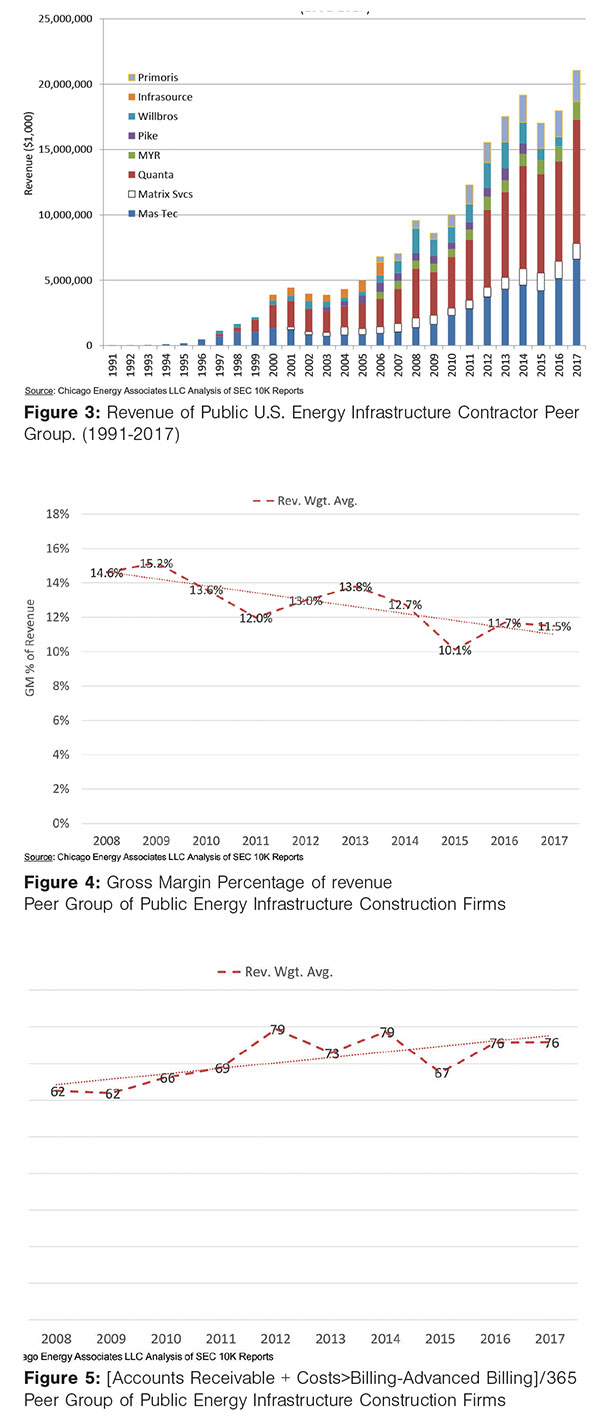

This analysis included the eight largest U.S. utility-focused contractors that have been variously or continuously publicly-traded since 1994 (Figure 2) and provides an invaluable window into the contractor’s world.

Utility construction contracting has historically grown side-by-side with the utilities industry. Like the T&D utilities they serve, the contracting industry is consolidating and consequently its large, publicly traded firms are performing an increasing portion of the U.S. infrastructure construction.

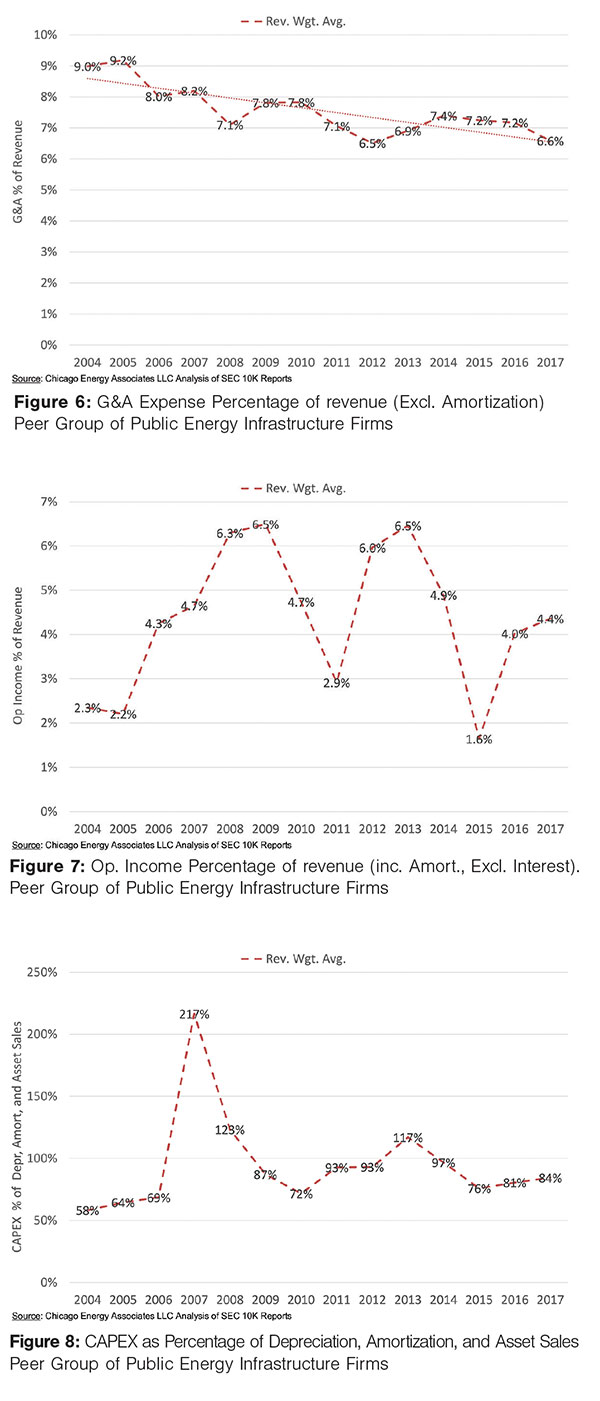

By 2017 these largest, publicly-traded firms have total revenue exceeding $20 billion annually (Figure 3). Because the utility T&D total capex (Figure 1) includes equipment, engineering, and rights-of-way (40-50% of total expenditures) and, similarly, these publicly traded contractors also have some non-energy T&D infrastructure business interests, their total share of the U.S. energy T&D construction market is now 20-25% and growing.

Substantially, all the public firms are growing significantly in the long run, both organically and by acquisition.

Moreover, the industry’s cyclical trends – the drop after Sept. 11, 2001 and the Enron debacle, the early 2000’s growth, the 2008 era financial crisis, the energy boom to late 2014, the 2015 oil price collapse, and the recent reacceleration of investment into 2017-2018 – are all apparent both individually and collectively for the industry. The bottom line is that utility T&D construction contracting is a growing, cyclical, competitive and consolidating industry.

Contractor Consolidation

Construction industry consolidation has had several important effects. These publicly-traded contractors are challenged by the equity markets to show strong, continuous growth regardless of macro conditions through both organic growth and acquisition. Their key organic growth levers include offering more aggressive pricing and pursuing ever larger construction contracts; both tactics have had negative effects on contractors’ gross margin percentage leading to a continuous decline since peaking before 2008-2009 (Figure 3).

This margin decline occurred during some years with significantly increasing demand. Overall, gross margin percentages levels have fallen about 20% in the past decade.

The corresponding impact of these tactics on their utility customers is also clear but less obvious to them. The industry’s gross margin percentage is the best reasonable proxy for the “markup” utilities paid contractors for the construction inputs of labor, materials, and equipment. It is at the lowest relative level of the past two decades and about 20% lower than the last peak around 2008-2009. Simply put, the current and recent levels of competition from consolidation have been good for utility T&D customers. There is little evidence that these contractors have much pricing power (i.e., margin percentage) at current levels of industry consolidation despite strong overall demand.

Additional evidence of this lack of market power also shows up in the average payment terms contractors realize from their utility customers. Contractors closely monitor their days sales outstanding (DSO) (Figure 5) as a business measure that integrates contract terms (e.g., advanced billing and unbilled costs) and customer payment performance (accounts receivable).

Industry average DSO has risen (i.e., degraded) about 20% over the past decade despite an era of strong customer demand and a consolidating industry of ever larger contractors.

This more aggressive pricing, lower margins, and tougher payment terms obviously weighs on all contractors. Fortunately, well-managed contractors can benefit significantly from economies of scale in their expanding businesses; growth has its advantages, too.

These scale economies are typically realized in their selling, general and administrative (G&A) expenses (Figure 6).

Over the past decade, the contractor industry’s G&A expenses as a percentage revenue have also declined, with the declines approaching the same 2.5-3% of revenue lost on their gross margin and with the gains skewed to the larger competitors.

The combined effect of these trends for America’s utilities can be stated succinctly: over the past decade contractors have aggressively grown and reduced average costs to their utility customers and they have enabled this cost (i. e. price) reduction by aggressively capturing economies of scale in their support operations and passing substantially all of these savings to their utility customers.

Working down the contractor industry’s Income Statement (Figure 7), the average operating income percentage (or profit percentage) for the large U.S. contractors is, in fact, rather dynamic year-to-year.

While it has varied between about 2% to 6. 5% of revenue since 2004, the levels are statistically unchanged over the long term. Experienced industry observers will certainly note how the larger profit patterns align most closely with coincident macro demand events – specifically, the sharp rise before the 2008 crisis, the decline in the immediate aftermath, the recovery era and rapid oil price increase that peaked in 2014 (and collapse thereafter), and the steady 2016-2017 recovery period. Thus, it is fair to conclude that contractor overall profits rise and fall with demand volume, but “mark-ups” paid by utilities for specific projects themselves have not increased.

The long-run average operating income percentage for the industry remains about 4%. It is historically a reasonable, long-run estimate for industry operating margin and consistent with a very competitive industry.

Stability of Industry

Taken together, there is compelling evidence that U.S. utilities build their energy T&D infrastructure by employing very aggressive contractors who offer declining relative prices and at slim overall profit level. Moreover, these contractors face tightening payment terms and carry the real construction risk.

Given this level of competition, it is also logical to question whether these contractors are continuing to invest in their businesses and, likewise, will these contractors be around for the long-term.

The construction industry’s average capital expenditures (predominantly on tools and equipment) is in about 90% (+/- 10%) of depreciation, amortization, and net asset sales over the long term (Figure 8) and very stable, thereby suggesting that the industry is continuing to reinvest at a historically strong rate.

Conclusions

Considering contractor operating income percentages presented in this article exclude interest and taxes, the long-run average net income after taxes in this highly competitive industry is about 3% overall.

U.S. utilities and customers benefit greatly from the diverse, aggressive and consolidating contractor industry that shoulders the expansive risks of developing complex construction projects at an almost tiny average profit potential. The industry as a whole has passed the benefits of their economies of scale back to their utility customers.

The reciprocal conclusions for contractors are equally sharp. Energy infrastructure contracting is highly competitive and long run success demands continued consolidation to drive economies of scale while simultaneously executing high-risk projects with excellence and innovation. These tough competitors remain committed to building the nation’s T&D infrastructure. P&GJ

Author: James M. Seibert is the managing partner of management consultancy Chicago Energy Associates LLC.

Comments