July 2023, Vol. 250, No. 7

Features

Global Construction Update: LNG Markets, Resurgent China Kindle Pipeline Projects

By Jeff Awalt, Executive Editor

(PGJ) — Global midstream markets continue to face near-term headwinds and economic uncertainties, but Europe’s rapid transition from Russian energy and projected higher demand in Asia continue to drive midstream expansion in those regions and others that supply them.

While macro-trends continue to favor growth in natural gas demand and infrastructure development, several factors have combined to depress pricing and threaten production growth during a period of shifting global trade. A milder-than-expected winter and unprecedented European conservation efforts have led to high natural gas storage levels in both Europe and the United States, contributing to a significant sell-off in natural gas prices during the first half of the year.

To a lesser degree, crude oil markets have also weakened in 2023 as recessionary trends and lower-than-expected demand from OECD countries combined with a slowdown in China’s demand recovery and a limited initial impact of Russian sanctions on export volumes. Announced OPEC+ production cuts and further effects of Russian sanctions and price caps, however, are projected to tighten markets and keep crude prices trending in the $75-$95 per barrel range for the rest of the year.

With energy security as a heightened concern, global pipeline construction activity continues to be positively impacted by Europe’s rapid shift away from Russian natural gas and toward LNG imports. The trends are not only influencing midstream projects in Europe, but also pipeline construction and expansion projects in North America and elsewhere.

Europe’s LNG Surge

Europe has moved with extraordinary speed to replace energy from Russia since its invasion of Ukraine, with some of the clearest indicators of this response seen in its rapidly expanding LNG import capacity.

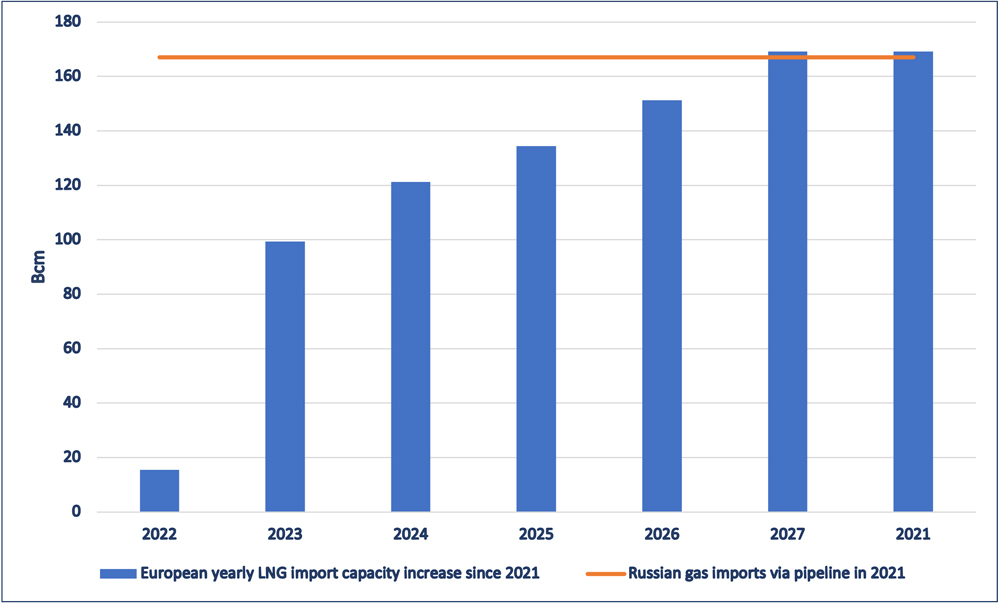

From the end of 2021 to the close of this year, Europe is on track for a 42% increase in LNG import capacity – an additional 73 mtpa. As the surge was starting last year, some analysts questioned whether Europe could have enough infrastructure in place to deliver the regasified LNG to where it would be needed. But Europe’s midstream industry has risen to the challenge with a series of natural gas pipeline projects linked largely to import volumes and focused on interconnectivity.

Europe’s yearly LNG import capacity is set to increase from about 15 Bcm in 2021 to more than 120 Bcm by the end of this year. That total is projected to increase to nearly 170 Bcm by 2026-27, surpassing the level of Russian gas imports in 2021. Among other countries, Greece, Italy, France, Poland and Ireland are looking to expand imports.

Germany

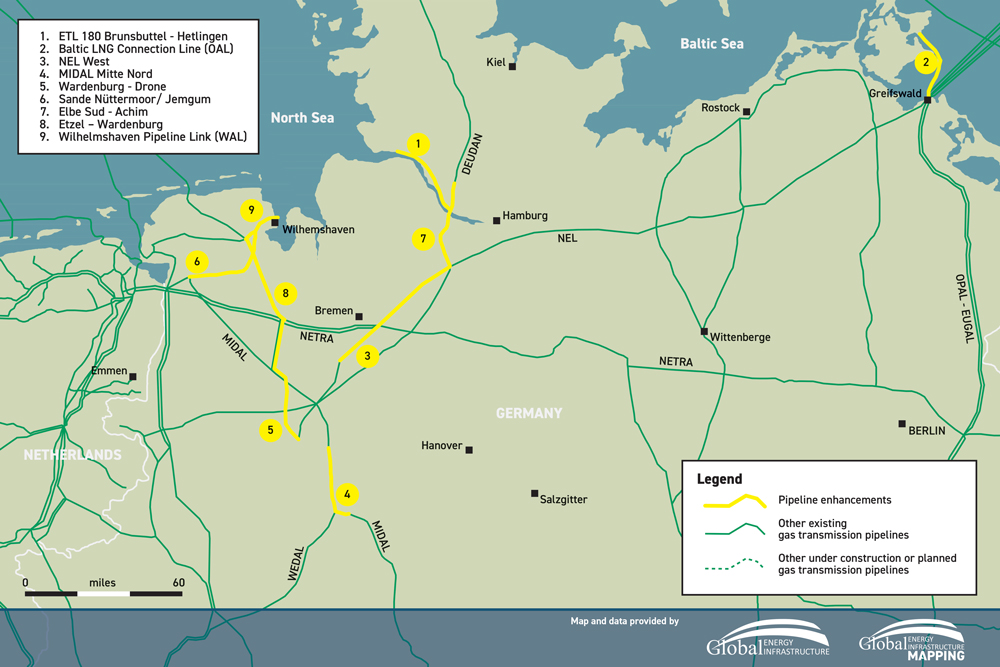

Germany, which had no operating LNG terminals before 2022, has been one of the most aggressive in pursuing rapid capacity additions by focusing on floating storage and regasification units (FSRUs). It leased four FSRUs in May 2022 capable of importing at least 5 Bcm of seaborne gas per year into Wilhelmshaven, Brunsbuttel, Stade and Lubmin. A fifth state chartered FSRU will be in Wilhelmshaven and is expected to be ready for winter 2023/24.

An additional four terminals are planned to begin operating by the end of 2027, and a fifth, large terminal is being explored for a location near Rugen. Collectively, these terminals represent 54 mtpa of LNG import capacity. This huge shift in gas sourcing is driving a change in the German gas transmission grid. In the 2022 draft German Plan for Gas Network Development, three new transmission pipelines associated with LNG flows are planned for completion in Germany by 2027.

Another project, the South Elbe-Achim pipeline, has been expanded from its original 2020 plan for a 32-inch pipeline to a 47-inch pipeline to accommodate the additional LNG terminals in Stade and Brunsbuttel. Gasunie is currently working on a new pipeline connected to the same terminals.

A pipeline connecting to the new terminals at Wilhelmshaven was completed in 2022, taking only nine months to move from the planning stage to completion. Other pipelines expected to support the smaller scale LNG imports Germany originally envisioned are also moving forward.

Collectively, nine German projects represent 333 miles of new pipeline. While not a huge increase in terms of length, all the pipe is high-capacity, with diameters 39 inches or wider – including 70 miles (112 km) of 55-inch pipeline. Four of these pipelines have been planned – and in the case of WAL Teil, built – since February 2022. A fifth project, the South Elbe-Achim pipeline, has been expanded from its original 2020 plans for a 32-inch pipeline to a 47-inch pipeline to accommodate the additional LNG terminals in Stade and Brunsbuttel.

If the proposed Rugen LNG terminal were to proceed, another pipeline would connect the planned Rugen LNG terminal to the grid. This 23-mile (37-km), 47-inch subsea Baltic pipeline would run adjacent to the Nord Stream pipelines and deliver gas from the large Rugen LNG terminal to the German gas grid. No start date for the terminal has been announced.

Poland

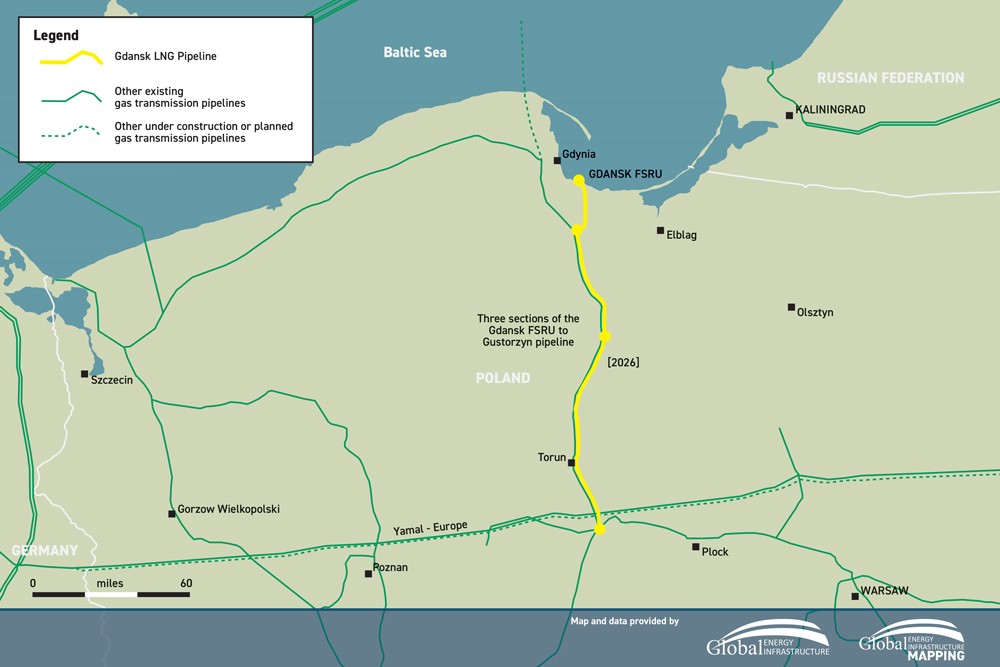

Poland is also adapting its gas grid to support new LNG imports. Three pipelines are being built to accommodate a new FSRU in the Gulf of Gdansk (G DANSK). Collectively, the (Kolnik-Gdansk, Gustorzyn-Gardeja and Gardeja-Kolnik) pipelines will add 155 miles (249 km) of 39-inch pipeline to Poland’s transmission system, carrying gas inland from the new 4.5-mtpa Gdansk FSRU. The pipelines are scheduled for completion in 2025 and 2026, with the FSRU expected to begin operation in 2027.

These pipeline projects in Poland and Germany reflect a broader midstream trend in northern Europe’s post-Russia era, with shorter, higher-capacity projects designed to pivot grids toward receiving gas from the coast to the North, rather than from the east, and make the most of existing grid capacities. Despite being designed to move regasified LNG to target markets they don’t always connect directly to LNG facilities or end users, instead they will de-bottleneck parts of the grid that will come under increasing pressure as the source of gas changes.

The projects are considered somewhat future-proofed. If LNG volumes don’t come to fruition or pipelines capacities are underutilized for some reason, developers may convert some natural gas pipelines to hydrogen or a mix.

Southern Europe

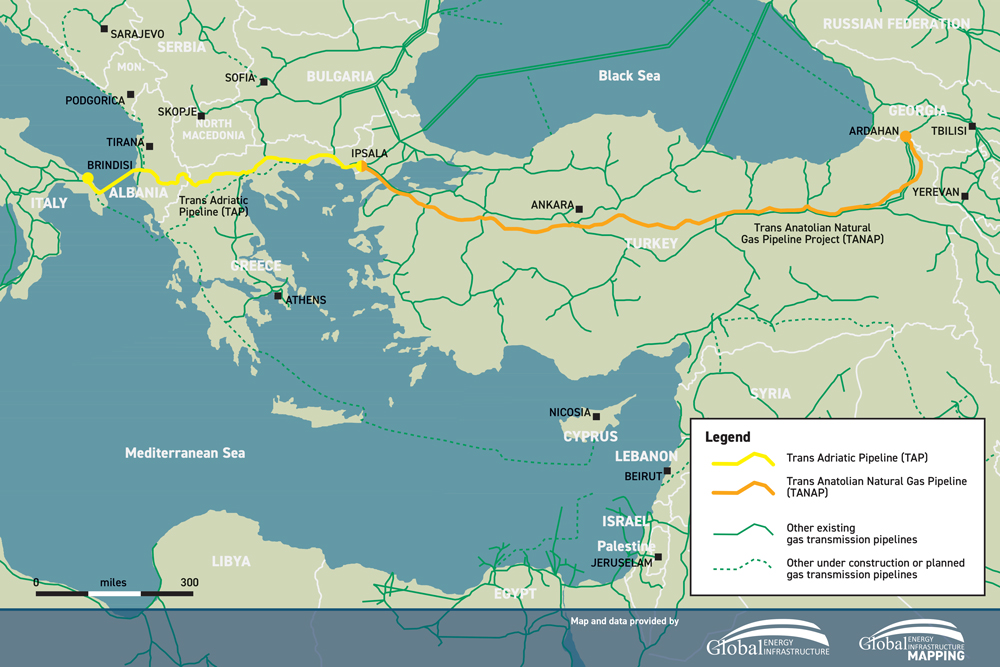

In the southeast, Europe is relying on increased supplies of gas from Azerbaijan. The TAP (Trans-Adriatic) and TANAP (Trans-Anatolian) pipelines form the southern gas corridor, carrying gas from Azeri gas fields across Turkey to Europe.

On Jan. 30, TAP triggered its first incremental expansion, which would grow capacity to 14.5 Bcm/y by 2026 via the addition of new compressor stations and upgrading existing ones. It was also announced that TAP was exploring options for a second stage expansion, again involving compressor stations, which could further increase capacity to 16.5bcm. TAP aims to increase capacity to 20bcm/y by the end of 2027.

TANAP also expects to expand further to accommodate increased gas flows to Europe. A planned two stage expansion would see the capacity of the pipeline increase to 24bcm/y and then 32bcm/y through the addition of five additional compressor stations.

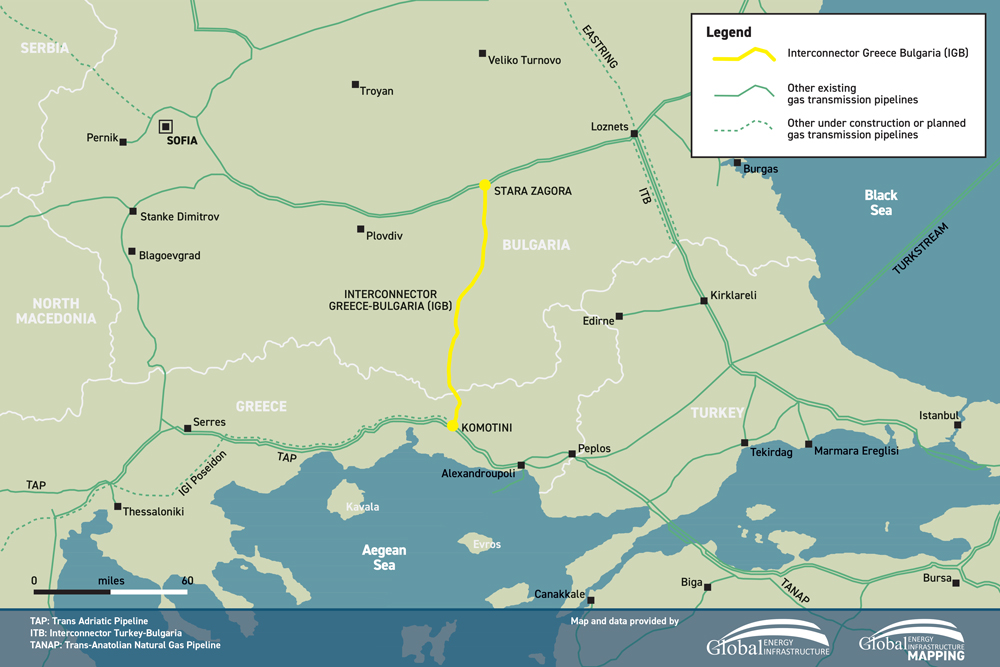

In 2021, Bulgaria counted on Russia for nearly 3 Bcm of its 3.3 Bcm annual gas consumption. The Interconnector Greece-Bulgaria (IGB) project began operations in October 2022 to better integrate the southeast Europe gas grid and flow Azeri gas north to Bulgaria. By early May of this year, more than 890 MMcm had been transported through IGB.

The 32-inch IGB pipeline has a capacity of about 3 Bcm/y and already supports the flow of 1Bcm/y of Azeri gas into Bulgaria. It will also be an important transport point for other countries in Europe looking to import gas from Azerbaijan. This year, Romania began receiving 1 Bcm/y of Azeri gas via the interconnector. Hungary is also looking to import Azeri gas, partially relying on the interconnector.

IGB operators plan to expand their capacity to 5 Bcm/y with the addition of a compressor station. Timing of the project is tied to completion of the Alexandropoulos LNG terminal near the Greek end of the pipeline by the end of 2023, expanding another source of non-Russian gas to southeastern Europe. The pipeline could also transport natural gas imported via Turkish LNG terminals into Bulgaria through a gas deal signed in 2023, although other pipelines do connect the countries.

Turkey is expected to have 26 mtpa of operational LNG import capacity by the end of 2023.

Eastern Mediterranean

The long-discussed East Med pipeline offers yet another option for diversifying gas supplies to Europe. The proposed 1,180-mile (1,899-km) East Med pipeline would be one of the longest and deepest in the world and provide an export route from Israeli and Cypriot gas fields in the East Mediterranean to European markets.

The estimated $6.4 billion (6 billion euros) project would transport up to 12 Bcm/y of natural gas across the Mediterranean to Greece, and then across the Adriatic to Italy via the associated Poseidon pipeline project. The design for the pipeline calls for 497 miles (800 km) of the structure to run offshore.

In late March, the Israeli, Greek and Cypriot foreign ministers announced the project was a priority, although the announcement was met with skepticism throughout the industry. More recently, Edison S.p.A plans to make the final investment decision on whether to support a pipeline delivering East Mediterranean gas to European by the end of this year, the Italian project developer told Reuters.

Because the project would guarantee an alternative to Russian supplies to Europe, Edison said, the European Commission could be interested in partly funding the project.

A potential alternative route would be to connect the offshore fields via Turkey, making use of the country’s existing pipeline network and avoiding most of the offshore sections of the pipeline, although no specific proposal along these lines has been made. This option faces political difficulties due to Turkey’s uncertain relationship with Israel and hostile relationship with Cyprus. If the pipeline were to move forward in either form, it would help secure an additional source of gas for Europe.

Asia-Pacific

China’s import pipelines

Just as Western Europe seeks to end its reliance on Russian energy imports, Russia has redoubled its efforts to expand into Asian markets by strengthening its alliance with China. But China is looking beyond Russia, and the speed of its economic recovery and extent to which its import demand will increase remain uncertain.

China’s LNG imports fell sharply in 2022 as its Zero COVID policy resulted in lockdowns of entire cities, followed by a wave of infections when they were suddenly lifted. Natural gas consumption is projected to increase as manufacturing and service sector activity rebounds, potentially tightening LNG supplies available to Europe this winter. Although growth projections have scaled back from earlier in the year, China is still widely projected to grow by an annual rate of 5% or more through the end of 2023.

Russia plans to construct the 1,615-mile (2,600-km) Power of Siberia 2 natural gas pipeline to transport up to 50 Bcm/a from its fields in the Krasnoyarsk and Irkutsk regions across Mongolia and into China. Gazprom is aiming to start delivering gas via the new pipeline by 2030.

While there are indications that it has agreed in principle on the project, China’s interest goes beyond its energy needs as seeks to broaden ties with Central Asia. Beijing is reportedly prioritizing Turkmenistan over Russia for its next major pipeline project and is seeking to accelerate development of the Line D project in support of its Belt and Road Initiative.

The 30 Bcm/a Line D pipeline, long delayed by financial and technical challenges, was estimated in 2014 to cost $6.7 billion. Speaking at a central Asian summit in March, Chinese President Xi Jinping urged leaders to prioritize laying Line D, almost a decade after the start of construction in Tajikistan.

It would be China’s fourth gas pipeline from the region. In 2022, China imported 35 Bcm gas via existing pipelines from Turkmenistan, compared with 16 Bcm through the Power of Siberia pipeline from Russia to northeastern China.

Also in China, Sinopec announced in April that it plans to build a 260-mile (400-km) pipeline to transfer hydrogen from renewable energy projects in its northwestern Inner Mongolia region to cities in its east, according to state media outlet Xinhua. The project would have an initial capacity of 100,000 tons per year, the report quoted Sinopec Chairman Ma Yongsheng as saying.

Asian LNG expansion

Demand for LNG continues to grow in other areas of Asia, creating additional competition for global supplies and potentially higher prices this winter. Hong Kong, Vietnam and the Philippines all become first-time LNG buyers this year.

The world’s largest FSRU arrived in Hong Kong in April to serve the city’s first LNG import terminal. The 4 mtpa import terminal project had been delayed by more than two years as the COVID-19 pandemic slowed construction. The FSRU is 345 meters long and has storage capacity of 263,000 cubic meters. It is a joint development of CLP Power Hong Kong Ltd and Hong Kong Electric Co. Ltd.

Also in April, AG&P International Pte. Ltd. said the Philippines’ first-ever LNG cargo arrived in the country, which is turning to imports to replace declining domestic gas production. AG&P converted the unit from an LNG carrier of ADNOC Logistics and Services under a 15-year deal signed with the Emirati company last year. ADNOC will supply LNG and operate and maintain the vessel under an 11-year charter with an option to extend it for four years.

In May, PetroVietnam Gas said it signed a contract to buy Vietnam’s first LNG cargo from Singapore-based Shell Eastern Trading. The cargo is for test running PetroVietnam Gas’s LNG terminal in the southern province of Ba Ria Vung Tau, the company said in a statement. The Thi Vai LNG Terminal will primarily supply two gas-fired power plants with a combined capacity of 1.5 gigawatts now being built in the neighboring province of Dong Nai by PetroVietnam Power Corp. at a cost of $1.4 billion.

Vietnam plans to develop a fleet of LNG-fired power plants with a combined capacity of 22.4 gigawatts by 2030, accounting for 14.9% of the country’s total power generation mix.

North America

In the United States, natural gas and crude oil production are on pace for record highs in 2023. While Permian natural gas production has seen little impact from sharply lower pricing, due to continuing oil production and high rates of associated gas, dry gas basins may see some reductions in the second half of the year.

Those near-term trends have had no apparent impact on midstream projects, however. More than 8 Bcf/d of pipeline capacity is either planned or under construction from the Permian and Haynesville basins as pipeline operators jockey for position around expanding LNG export markets on the Texas and Louisiana Gulf Coasts.

Permian gas pipelines

While most of the Permian Basin natural gas pipelines built in recent years have targeted LNG export markets south of the Houston area, two proposed intrastate natural gas pipeline projects have emerged within the past six months to a goal of delivering Permian Basin gas to the Texas-Louisiana border region.

The larger of the two, Targa’s 562-mile (847-km) Apex pipeline, was approved by the Railroad Commission of Texas in late March. It would originate in Midland County in West Texas to Jefferson County, along the Louisiana border near Sabine Pass.

WhiteWater Midstream’s proposed 190-mile (306-km) greenfield Blackfin Pipeline, which filed for state regulatory approval in February, takes a different approach. Although Blackfin would originate at the eastern edge of the Eagle Ford shale, it would primarily serve as an extension of the 580-mile (933 km) Matterhorn Express Pipeline that was sanctioned in May 2022 by a joint venture of WhiteWater, EnLink Midstream, Devon Energy and MPLX.

The greenfield Matterhorn Express is scheduled to be in service in the third quarter of 2024 and will provide 2-2.5 Bcf/d of Permian takeaway capacity to the Katy area west of Houston. Blackfin would link with Matterhorn to help debottleneck the Katy area and, like Apex, deliver volumes east to the Texas-Louisiana border area.

The two other natural gas capacity expansions out of the Permian are being accomplished via compressor expansions, which can increase capacity quickly, but at a higher operating cost, because squeezing out that extra deliverability with higher compression requires more fuel. Since fuel rates are based off a percentage of product prices, the downturn in natural gas prices since last year’s highs will bring some cost benefit.

WhiteWater announced in May 2022 that it would expand the Whistler Pipeline’s mainline capacity through the installation of three new compressor stations. The new compressor stations will increase the pipeline’s mainline capacity by 500,000 MMcf/d, to 2.5 Bcf/d from 2 Bcf/d). The expansion is scheduled to be in service in September 2023. The Whistler Pipeline is owned by a consortium including MPLX, WhiteWater and a joint venture between Stonepeak and West Texas Gas, Inc.

Kinder Morgan’s Permian Highway Pipeline (PHP) expansion project has been sanctioned to increase capacity by 550 MMcf/d. The project adds compression on PHP to increase natural gas deliveries from the Waha area to multiple mainline connections and Gulf Coast markets. Kinder Morgan has noted supply chain issues are resulting in delays and expects startup in December 2023.

While most of the Permian’s natural gas projects aim father east to Gulf Coast LNG markets, there is also an appetite for Permian gas to fuel LNG exports from the West Coast of Mexico primarily to Asian markets.

ONEOK filed a Presidential Permit application with the Federal Energy Regulatory Commission (FERC) in December 2022 to construct its proposed Saguaro Connector Pipeline for natural gas export at a new Mexican border crossing in Hudspeth County, Texas. The 2.8 Bcf/d project from the Waha hub would extend 155 miles (250 km) to the border, where it would connect with an as-yet unannounced Mexican pipeline to that country’s west coast.

The Mexican pipeline would deliver Permian gas to a New Mexico Pacific Limited LNG liquefaction and export facility, recently renamed Saguaro LNG. In addition to the shorter distances for cargoes to travel to LNG-hungry Asian markets, the development of LNG export facilities on Mexico’s West Coast would also avoid the crowded Panama Canal.

Haynesville gas corridors

The primary driver of U.S. natural gas demand growth is LNG exports, and outside of the Permian Basin, that growth and its associated midstream projects are concentrated in the Haynesville shale of northern Louisiana and Northeast Texas.

Energy Transfer has already finished construction of the 1.65 Bcf/d Gulf Run pipeline to move gas from north Louisiana to the coast. That project, which Energy Transfer gained via its acquisition of Enable Midstream in December 2021, is backed by a 20-year agreement with the $10 billion Golden Pass LNG export plant now under construction in Texas by QatarEnergy (70%) and Exxon Mobil (30%).

There are currently a half-dozen natural gas pipeline projects in various development stages to connect Haynesville gas producers in the north to Gulf Coast LNG exporters to the south – that is, if the three-stages of DT Midstream’s Louisiana Energy Access Pipeline (LEAP) expansion are counted separately.

The existing LEAP Gathering Lateral Pipeline is a 155-mile, 1 Bcf/d line stretching from the Haynesville to the Gulf Coast region. DT midstream plans to increase LEAP capacity by 90% through compression and construction expansions to 1.9 Bcf/d. The three phases include a 300 MMcf/d addition with expected in-service by the end of this year, a 400 MMcf/d expansion due online in the first quarter of 2024 and a final 200 MMcf/d due in the third quarter of next year.

Momentum Midstream is currently developing the New Generation Gas Gathering project, dubbed NG3 from the Haynesville to coastal Louisiana LNG markets, with 275 miles of additional natural gas gathering pipelines with 2.2 Bcf/d of capacity. The system will be complemented with a carbon capture and sequestration (CCS) solution to offer producers a net negative CO2 emission solution. NG3 is expected to be completed in 2024.

Williams announced in May 2022 that it was committing around $1.5 billion to expand natural gas capacity and grow market access and followed up a month later by sanctioning its Louisiana Energy Gateway (LEG) project, which is designed to move 1.8 Bcf/d of Haynesville natural gas to several Gulf Coast markets, including interconnection with its Transco gas pipeline from Texas to the U.S. Northeast, as well as industrial consumers and Gulf Coast export plants. Tulsa-based Williams expects start-up of the LEG system by 2024.

Rare Marcellus win

Natural gas pipeline capacity out of the U.S. Northeast has grown every year since 2014, but it has failed in recent years to keep pace production growth, resulting in bottlenecks and stagnant production from the gas-rich region.

During the past six years, five major pipeline projects that were designed to ship Appalachian gas to East Coast markets have been canceled, for the most part due to regulatory impasses and associated costs. A recent exception is the 303-mile (487-km) Mountain Valley Pipeline (MVP) from the Marcellus shale, under development by Equitrans Midstream and NextEra Energy.

Although already 94% complete, it literally took an act of Congress to finally clear the path this year for MVP’s completion. On June 3, President Joe Biden signed legislation that raised the nation’s debt limit and ratified and approved all permits and authorizations necessary for the construction and initial operation of MVP.

The legislation directs federal agencies to maintain such authorizations and requires the Secretary of the Army to issue all permits or verifications necessary to complete project construction and allow for MVP’s operation and maintenance.

Given the legislation, and assuming the timely issuance of the few remaining authorizations, Equitrans said it intends to work with its project partners to complete construction of MVP by year-end 2023, at an estimated total project cost of approximately $6.6 billion.

Comments